Moody’s Downgrade: The US Just Lost Its Gold Star, Now What?

What it means when America drops from AAA to Aa1, why the bond market cares more than your stock portfolio, and how it might mess with your mortgage.

“US Credit Rating Downgraded” is one of those headlines that just sounds terrifying. It’s been making the rounds after Moody's downgraded the credit rating of the United States from AAA to Aa1, which is still high, but not quite the gold star we used to have. (A solid write-up on this can be found here.)

So, what does this actually mean? Let’s unpack the who, why, and what I think it all means.

Important disclaimer: This is just one guy’s opinion. I’m not an economist, just someone who pays close attention to the economic markets.

Buckle up as we go on a super-nerdy economic journey, think Lord of the Rings, but with fiscal policies instead of swords, spreadsheets instead of magic scrolls, and a fellowship of cardigan-wearing economists guiding the way. Yeah, that nerdy.

Don’t worry, I’ll be back to motivation, real estate tactics, and strategy soon. Probably Thursday.

OK, off we go.

Context

This news would tend to impact the bond market more than the stock market. Since the bond market is (basically) selling confidence that the United States can pay back the notes they’re putting out, the bond market will be much more sensitive to this news. This is (or could be) more of a bond story than a stock market story, at least for today.

Who: What’s Moody’s Deal?

Let’s start with Moody’s, since they made the downgrade and the headline.

Moody’s Corporation is like the financial world’s strict-but-fair (depending on who you ask on the fair part) high school teacher who grades everyone’s homework, except the “homework” is billions of dollars in debt, and the “students” are countries, corporations, and banks. If you’re doing great, you get an Aaa; if you’re about to flunk (i.e., default), you’re getting a C and a long talk with the principal (aka investors).

Historical Context

It is news that Moody’s has downgraded the US rating, but the two other big rating agencies have already done it, one of them a looooonnng time ago.

Standard & Poor's made its first-ever downgrade in 2011, which was on the heels of the Great Recession. Fitch Ratings followed in 2023 for basically all the reasons Moody’s did, which we’ll cover in the “why” portion below.

Market Reactions

The stock market shook it off easily. Which you would think is a little odd. Like the third of three big rating agencies cut the US credit worthiness, it shouldn’t be a non-event. But (so far) it has been.

Why? I think this is an example of what they’d call “baked in”. Meaning because of the two other rating agencies and the amount of conversation on the US deficit, so the market is kinda saying “Duh… this isn’t news folks.”. But the bond market, understandably did react on the news.

We saw about a 15 basis point move in the 10-year treasury, which is a pretty big move. But it did hit a ceiling and then start a pretty strong retrenchment back down. This will mean interest rates for mortgages will be on the rise, in the news, and you can see it clearly reflected in this chart, and then the recovery. The word for the day is volatility, kids, prepare for it.

Why Did They Do It?

Short answer: The U.S. deficit.

I’ve written a lot about the looming problem that the deficit is. One of these days, I’ll do a full write-up on the debt spiral that has ended many a global power throughout history and the trajectory the United States is on.

But it's a beautiful Tuesday, and I don’t want to tell any horror stories today.

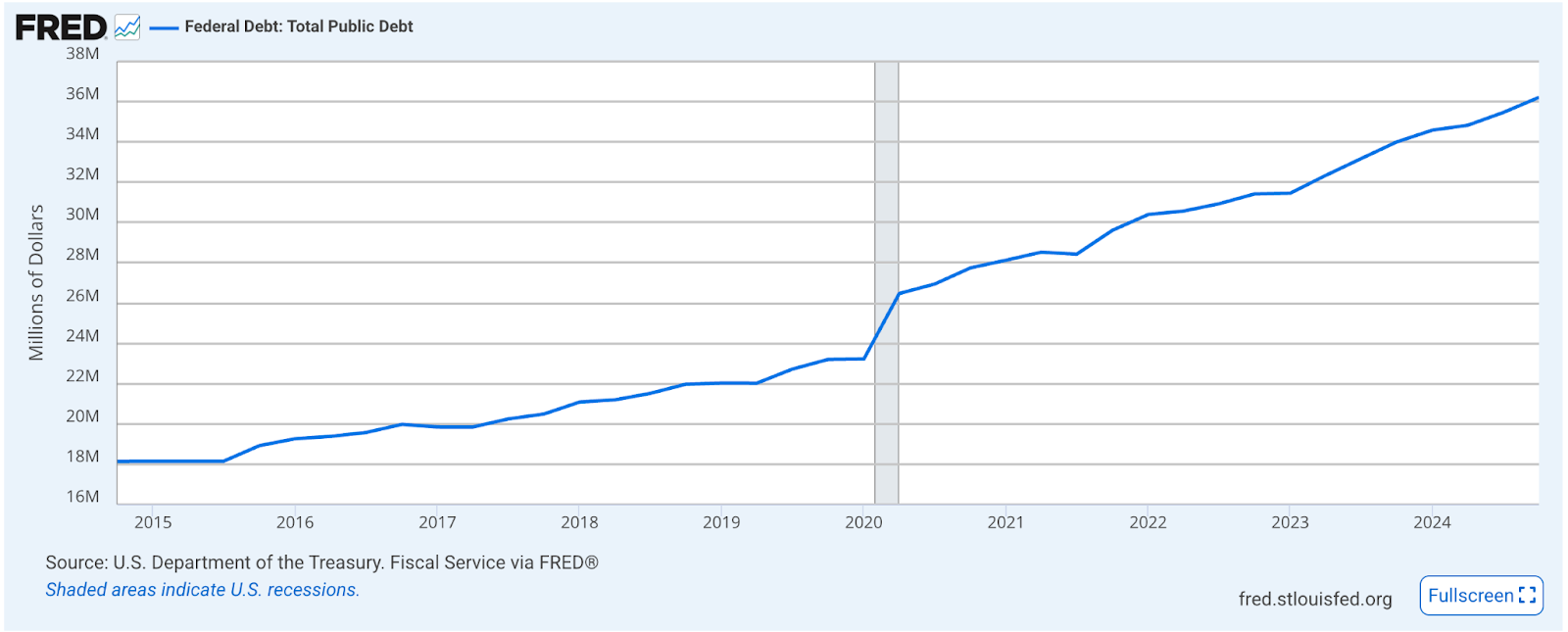

The below graph pretty much lays it out. You can see the trend line since 2015, which shows the Federal Debt. (yuck) You can also see in the gray bar the bump up just after 2020 during the COVID spending. From there, it really takes off with no signs of slowing down.

Simply put, this is marching up and to the right, which isn’t a good thing when you’re talking about debt. With no signs of slowing. This is why the bond market is skittish, evoking vigilante-ism (more on this at the end) and remaining as sticky as that gum under the desk in middle school (also yuck) to the high side.

What Does This Mean?

1. Stickier, Higher Interest Rates

Sadly, real estate fam, this is exactly what we don’t need right now. I keep feeling like we get close to the bond market finally capitulating to lower rates, and then we get some kind of news like tariffs, Moody’s downgrade, or something else.

I’m not blaming this on the media per se, I just mean we can’t seem to get to a “normalized” market. But the short answer to what happens when something is more risky (lower credit rating) the investors will demand a higher return. More risk, more return, which means higher rates for folks looking to borrow money for a house.

2. The “Cleanest Dirty Shirt”

This is a common refrain in economic circles. It’s a kinda messy but effective analogy to describe why folks keep investing in the United States.

Sure, it may be having its problems, deficits are super high, but when folks look around the globe, the US is still the best place to invest if you’re looking for quality and safety.

Maybe a lower quality than “before” (whatever that is), but most of the globe is having some kind of economic issues, making the US the “cleanest dirty shirt”. This is one of the reasons why the markets (both stock and bond) didn’t move radically on the news.

3. Dollar Dominance (Nerd Level 10,000)

This one could be its own newsletter, which would be like nerd level 10,000. So I am just going to keep it short and link to a longer article if you really want to dig in, but let's just say this, there is a real value in being the currency everyone wants to hold/trade in when they’re doing stuff globally. And that is what the dollar is. A longer write-up can be found here.

My Final Thoughts

We’re over 1,000 words on bonds and credit ratings, so I'd better wrap this up before y’all start hitting unsubscribe like Netflix users dodging the ‘Are you still watching?’ screen after a 12-hour binge.

Mostly, I am just frustrated, probably like many of you reading. I hate to just pound on the keyboard and talk about interest rates. I’d much rather talk about the value an agent brings and how we change lives. But sometimes we have to understand what is going on in the markets so we can be the voice in our local markets.

I promise a lot of folks are going to be wondering “What in the hell does all this Moody’s stuff mean??”. You have to be the voice in your local market, telling them. Or heck, just share what I wrote with a quick summary or thoughts on what I wrote.

You don’t have to be the expert, you just have to know where to find them. If you get nothing else, get that your people in your local markets need you to translate this stuff for them, and the more you can do that, the more memorable you’ll be.

It will shift. I don’t know when. But when it does, the people with the most audience and the people who have been the “voice” in their local area or groups will get their unfair share.

-k

Like nerdy economic breakdowns with just enough snark to keep it interesting? Subscribe below and let’s ride the waves of market madness together.